Understanding Disability Insurance: What You Need to Know

Disability insurance is a crucial financial safety net that provides income replacement in the event that you are unable to work due to a disabling condition. This type of insurance is essential for safeguarding your financial future, as it ensures that you can maintain your standard of living even in the face of unforeseen circumstances. It's important to understand the different types of disability insurance available, including short-term and long-term options, so you can choose the coverage that best suits your needs.

When considering disability insurance, there are several key factors to keep in mind:

- Elimination Period: This is the waiting period before benefits begin, which can vary significantly.

- Benefit Period: This refers to the length of time you will receive benefits if you become disabled.

- Coverage Amount: Assess how much of your income will be replaced, typically ranging from 50% to 70%.

5 Common Misconceptions About Disability Insurance Debunked

Many individuals harbor misconceptions about disability insurance, leading them to forgo this essential coverage. One prevalent myth is that disability insurance is only necessary for high-risk professions. In reality, accidents and illnesses can happen to anyone, regardless of their job. Another misconception is that disability insurance provides coverage only for catastrophic events; however, short-term disabilities — such as surgery recovery or a serious illness — can also lead to significant income loss, making adequate coverage vital. Furthermore, some believe that their employer's policy is sufficient, but employer-sponsored plans often lack the comprehensive protection needed in personal circumstances.

Additionally, many people think that disability insurance payouts will cover their entire salary. Contrary to this belief, most policies replace only a percentage of your income, generally ranging from 50% to 70%. This misunderstanding can lead to financial strain if individuals are not prepared for a reduced income during their recovery. Lastly, a common myth is that obtaining disability insurance is a complicated process fraught with red tape. In fact, with online platforms and simplified applications, securing coverage has become more accessible than ever. Debunking these common misconceptions about disability insurance is essential for making informed decisions about financial protection.

Is Disability Insurance Worth It? Here’s What You Should Consider

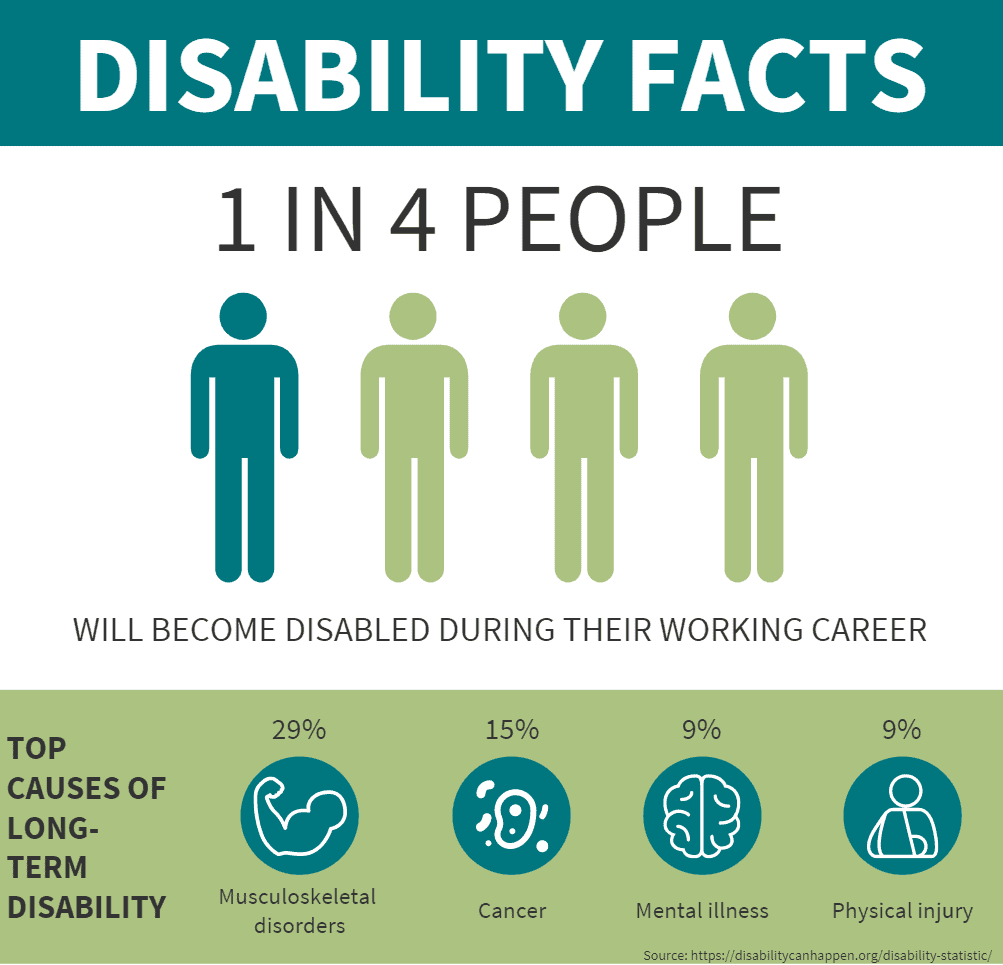

When considering whether disability insurance is worth it, it's crucial to evaluate your personal circumstances and financial situation. This type of insurance provides income replacement if you become unable to work due to a disability. According to statistics, about one in four individuals will face a disability during their working years. With this in mind, you should assess your current savings, expenses, and whether you have a safety net to cover your living costs in case of a sudden loss of income.

Another important aspect to consider is your occupation and the likelihood of experiencing a work-related injury or illness. For instance, if you work in a physically demanding job, the risk of disability might be higher than for someone in a desk job. Additionally, consider the cost of disability insurance premiums versus the financial impact that a potential loss of income could have on your life. Speaking with a financial advisor can help you determine if this insurance aligns with your long-term goals and provides peace of mind in your financial planning.